The DeFi Metric Everyone Gets Wrong—And How It Can Cost You

TVL is the DeFi metric everyone watches but nobody fully understands. Here's why high TVL doesn't equal safety, profit, or long-term success—and what really matters.

You’ve seen the charts. A crypto analyst points to a skyrocketing line and declares a DeFi protocol the next big thing. That line is almost always Total Value Locked, or TVL. It’s the headline number for an industry that now claims to secure over $3.11 trillion across all blockchains as of September 2025. But what if I told you this metric is one of the most misleading signals in finance? What if blindly trusting it is the fastest way to get burned?

Insights

- Total Value Locked (TVL) is the total dollar value of all assets deposited into a decentralized finance protocol's smart contracts. It’s a measure of the capital base.

- It’s often compared to Assets Under Management (AUM) in traditional finance, but TVL is unregulated, self-reported, and riddled with inconsistencies.

- The calculation sums the USD value of each distinct asset locked in a protocol. It is not a simple multiplication of a single token's count and price.

- A high TVL does not mean a protocol is profitable, secure, or a good investment. Recent studies confirm TVL has no predictive power for token outperformance.

- You must look past TVL and analyze revenue, user growth, security audits, and the risk of double-counting to make a sound judgment.

What Exactly Is Total Value Locked?

Let’s cut through the noise. Total Value Locked (TVL) represents the total value, in U.S. dollars, of all the crypto assets currently sitting in a specific DeFi protocol. These assets are the fuel for the system—they could be staked to earn rewards, supplied to a lending market, or deposited into a liquidity pool on a decentralized exchange.

It’s the first number most people look at. It’s also the first place they go wrong.

TVL can be measured for a single protocol, like Aave, or for an entire blockchain ecosystem, like Solana. But be warned: aggregators often double-count assets that are used across multiple protocols, painting a deceptively large picture of the capital at play.

The Flawed Comparison to Traditional Finance

People love to call TVL the DeFi equivalent of Assets Under Management (AUM). It’s a neat comparison, but it’s lazy and dangerous. A mutual fund’s AUM is governed by strict regulatory and reporting standards. It’s audited. It’s verified.

TVL is the Wild West. It’s an open, often self-reported metric that can be easily manipulated. While AUM tells you how much capital a trusted manager is directing, TVL just tells you how much money is sitting in a set of smart contracts, without any context on its safety, efficiency, or profitability.

"TVL is essentially the DeFi equivalent of assets under management in traditional finance, showing how much capital is being put to work in protocols like lending, staking, or liquidity pools."

Andre Cronje DeFi Architect and Founder of Yearn Finance

How the Number Gets Calculated

The math seems simple on the surface. To find a protocol's TVL, you sum the current market value of every single token locked in its smart contracts. The final number is almost always shown in USD to make comparisons easier.

For instance, if a protocol holds 100,000 DAI (worth $1 each) and 10,000 ETH (with ETH at $3,200), its TVL would be calculated as ($100,000) + (10,000 * $3,200), for a total of $32,100,000.

This direct link to asset prices is a critical weakness. A protocol's TVL can collapse overnight not because users are fleeing, but simply because the price of its primary asset got crushed in the market.

Where to Find TVL Data (And Why You Shouldn't Trust It Blindly)

Data aggregators like DeFi Llama, DappRadar, and Token Terminal are the go-to sources. They pull data directly from blockchains to create dashboards that track value across thousands of protocols. As of September 2025, for example, DefiLlama reports around $127 billion locked in DeFi protocols globally.

But these numbers come with a massive asterisk. Methodologies differ, and the problem of double-counting assets is rampant.

"DeFi Llama, DappRadar, and Token Terminal are the primary sources I use to track TVL data across protocols and chains, but always be aware of potential double-counting in these aggregators."

Lucas Campbell Head of Web3 at Bankless

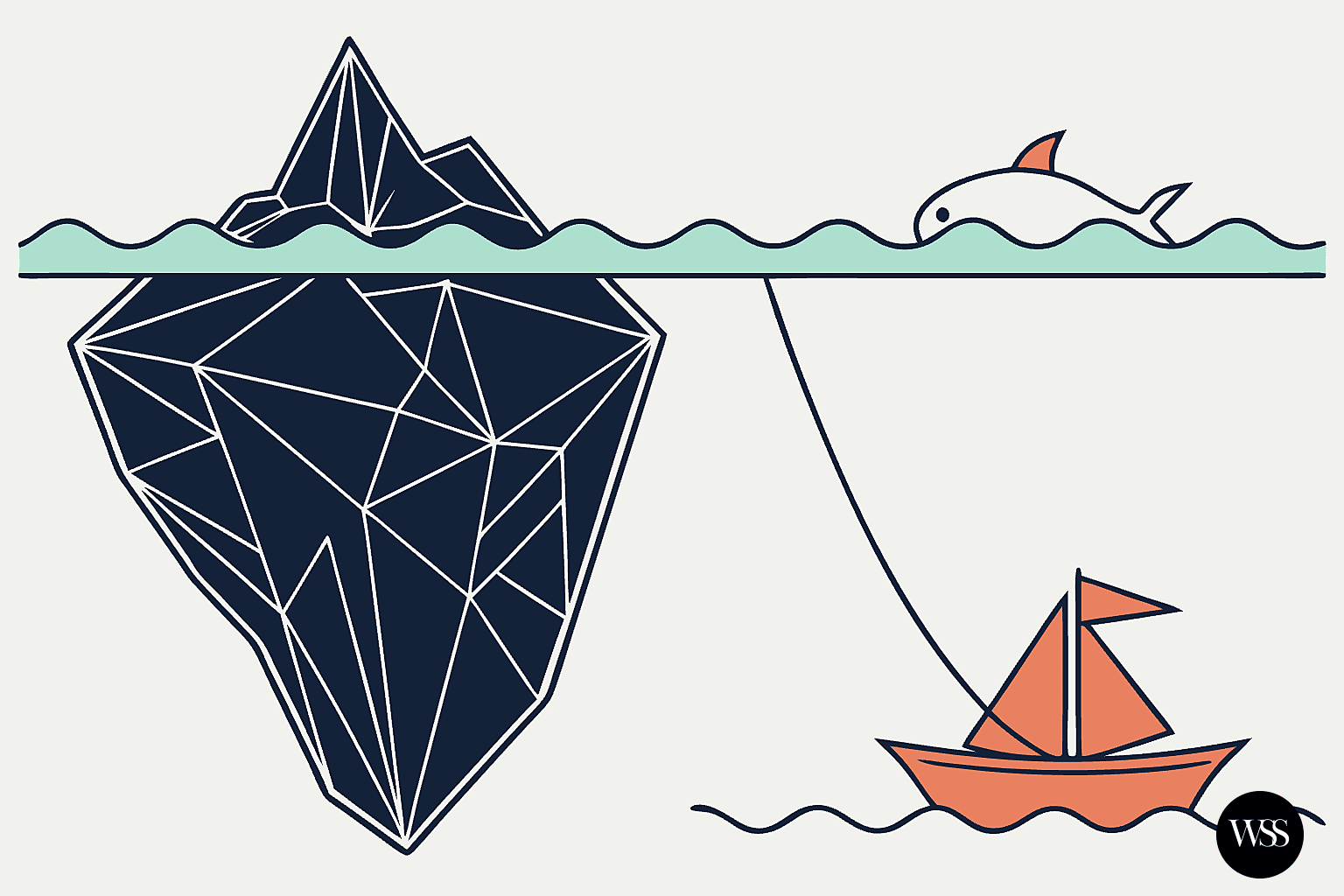

Warning: TVL Is a Vanity Metric, Not a Sign of Health

Here’s the hard truth: a high TVL means very little on its own. It’s a measure of capital, not a measure of success. A protocol can have billions in TVL and still be unprofitable, insecure, and on the verge of collapse.

Think of a bank with billions in deposits that isn't making any profitable loans. The deposits look impressive, but the business is failing. The same logic applies here. Recent research from 2025 confirms that portfolios built around high-TVL protocols generate no excess returns. It is not a predictor of performance.

"TVL is a useful metric, but it’s not the only one you should look at—high TVL doesn’t necessarily mean a protocol is profitable or safe."

Kain Warwick Founder of Synthetix

The Yield Farming Trap: How TVL Gets Manipulated

Protocols can easily juice their TVL by offering absurdly high, unsustainable yields. This attracts waves of "mercenary capital"—funds that rush in to farm the rewards and will disappear the second those incentives dry up.

This creates a mirage of growth and adoption. The TVL chart goes vertical, social media buzzes, and naive investors pile in, assuming the project is a winner. In reality, they're just providing exit liquidity for the mercenaries.

"TVL can be manipulated by protocols offering unsustainable yields to attract short-term capital, so it’s important to look at other indicators like user activity and revenue."

Tarun Chitra Founder and CEO of Gauntlet

The Hidden Flaw of Double-Counting

One of the biggest structural problems with TVL is double-counting. A liquid staking token like Lido's stETH is a perfect example. The original ETH is counted once in Lido's TVL. Then, when a user takes that stETH and deposits it as collateral in Aave, it gets counted a *second time* in Aave's TVL.

This inflates the total TVL of the entire ecosystem, giving a false sense of the actual, unique capital that has entered the system. Studies in 2025 revealed that only about 46.5% of protocols' reported TVL figures align with fully verifiable on-chain data. The rest is murky.

Analysis

The obsession with TVL is a symptom of an immature market looking for a simple scorecard. In traditional markets, we analyze price-to-earnings ratios, revenue growth, profit margins, and free cash flow. In DeFi, many have settled for a single, flawed number that measures capital attraction, not business viability.

A high TVL doesn't mean a protocol has found a product-market fit. It often just means it's offering the highest subsidy. The real questions you should be asking are different. How much revenue is the protocol generating from its TVL? What is its profit margin? Are its users sticky, or will they flee when the yield drops? Has it undergone rigorous, repeated security audits?

A lending protocol like Aave, with a TVL of around $12 billion, is only successful if a healthy portion of that capital is being borrowed, generating fees that outweigh expenses. A decentralized exchange like Uniswap, with a TVL of $5 billion, is only valuable if that liquidity is facilitating high trading volume, which in turn generates fees for its liquidity providers and the protocol.

The market is slowly waking up to this. Efforts to standardize reporting through concepts like "verifiable Total Value Locked" (vTVL) are a step in the right direction, aiming to provide a more transparent, on-chain source of truth. But until these become standard, you are navigating a minefield. Treating TVL as your north star is a critical error. It's a single data point on a very complex map, and it often points in the wrong direction.

Final Thoughts

Stop looking at TVL as a finish line. It’s a starting point, and often a deceptive one. It tells you that capital is present, but it tells you nothing about the quality, security, or sustainability of the protocol holding it. A rising TVL can be a sign of genuine growth, or it can be a signal of a temporary, high-risk subsidy game that’s about to end badly.

The smart money in this space has already moved on. They pair TVL with deep dives into user activity, transaction volume, protocol revenue, and the strength of the developer community. They treat a high TVL not as a reason to invest, but as a reason to start asking much harder questions.

Your job as an investor is to separate the signal from the noise. In DeFi, TVL is almost always noise.

"Total Value Locked, or TVL, is the sum of all assets deposited in a DeFi protocol’s smart contracts, and it’s become a key metric for measuring the health and adoption of decentralized finance."

Stani Kulechov Founder and CEO of Aave

Did You Know?

In response to the widespread issue of inaccurate and inflated TVL figures, a new standard known as "verifiable Total Value Locked" (vTVL) was proposed in 2025. This initiative aims to create a transparent and standardized method for calculating TVL directly from on-chain data, reducing the reliance on third-party aggregators and eliminating common issues like double-counting.